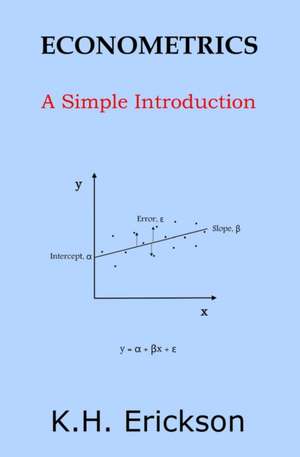

Econometrics: A Simple Introduction

Autor K. H. Ericksonen Limba Engleză Paperback

Preț: 77.71 lei

Nou

14.87€ • 15.47$ • 12.28£

Carte disponibilă

Livrare economică 22 martie-05 aprilie

Specificații

ISBN-10: 1496013867

Pagini: 102

Dimensiuni: 133 x 203 x 5 mm

Greutate: 0.11 kg

Editura: CreateSpace Independent Publishing Platform

V-ar putea interesa

-

Econometric Methods with Applications in Business and EconomicsChristiaan Heij-20%Preț: 649.49 lei814.86 lei

Econometric Methods with Applications in Business and EconomicsChristiaan Heij-20%Preț: 649.49 lei814.86 lei -

Econometric Modeling – A Likelihood ApproachDavid F. Hendry-19%Preț: 627.73 lei774.98 lei

Econometric Modeling – A Likelihood ApproachDavid F. Hendry-19%Preț: 627.73 lei774.98 lei -

Analysis of Economic DataG KoopPreț: 399.79 lei

Analysis of Economic DataG KoopPreț: 399.79 lei -

Econometric Analysis, Global EditionWilliam H. Greene-13%Preț: 518.72 lei596.23 lei

Econometric Analysis, Global EditionWilliam H. Greene-13%Preț: 518.72 lei596.23 lei

Descriere

Econometrics: A Simple Introduction offers an accessible guide to the principles and methods of econometrics, with data samples, regressions, equations and diagrams to illustrate the analysis. Examine a linear and multiple regression model, ordinary least squares method, and the Gauss-Markov conditions for a best linear unbiased estimator. Understand hypothesis testing, with a null hypothesis, t, F or chi-square test statistics and distributions, and interpret regression results. Dummy variables model qualitative data and Chow tests assess regression equivalence. Explore heteroscedasticity with the White method and with generalized least squares, Goldfeld-Quandt, Breusch-Pagan, and White tests. Assess autocorrelation with Durbin-Watson, Durbin h, and Breusch-Godfrey tests, lagged variables and auxiliary regressions. Assess the impact of omitted variables, incorrect variables or functional form, and a non-normal distribution with Ramsey RESET and Jarque-Bera tests. Model random variables with the Method of Moments' estimators, instrumental variables and Hausman test.