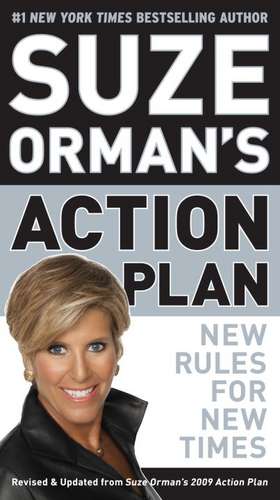

Suze Orman's Action Plan: New Rules for New Times

Autor Suze Ormanen Limba Engleză Paperback – 28 feb 2010

There is a new reality out there—a new normal. What was once certain—that you would be able to retire comfortably, that you would pay for your kids’ education, that your home would appreciate in value—is no longer a sure thing. So much has changed on the financial landscape that it’s hard to know which moves are the right ones to make. Suze Orman’s million-copy bestselling financial action plan—fully revised and updated for 2010 and beyond—will show you the way.

NEW TIMES CALL FOR NEW RULES—AND THIS IS WHAT SUZE ORMAN’S ACTION PLAN DELIVERS:

• up-to-date information on new legislation that could affect how you will achieve your financial goals

• an explanation of new FICO practices, and a new strategy for dealing with credit card debt

• sound advice about rebuidling your retirement plan, and what to do if you’re already retired

• guidance on how to live within your means, and strategies to keep you on the path to achieving your goals in this new age of financial honesty

PLUS AN ALL-NEW CHAPTER ON KIDS AND MONEY—how to give your kids a solid financial education, no matter their age!

Download Suze Orman’s free Money Tool iPhone applicaton in the iTunes store.

Preț: 56.50 lei

Nou

Puncte Express: 85

Preț estimativ în valută:

10.81€ • 11.56$ • 9.01£

10.81€ • 11.56$ • 9.01£

Carte disponibilă

Livrare economică 27 martie-10 aprilie

Livrare express 12-18 martie pentru 15.80 lei

Preluare comenzi: 021 569.72.76

Specificații

ISBN-13: 9780812981551

ISBN-10: 0812981553

Pagini: 244

Dimensiuni: 108 x 193 x 17 mm

Greutate: 0.14 kg

Ediția:Revised, Update

Editura: Spiegel & Grau

ISBN-10: 0812981553

Pagini: 244

Dimensiuni: 108 x 193 x 17 mm

Greutate: 0.14 kg

Ediția:Revised, Update

Editura: Spiegel & Grau

V-ar putea interesa

-

Preț: 106.42 lei

Preț: 106.42 lei -

HomefactsLifestyle Publishing CompanyPreț: 121.45 lei

HomefactsLifestyle Publishing CompanyPreț: 121.45 lei -

Preț: 116.01 lei

Preț: 116.01 lei -

Women & MoneySuze OrmanPreț: 139.84 lei

Women & MoneySuze OrmanPreț: 139.84 lei -

Busting the Retirement LiesKim D. H. ButlerPreț: 68.91 lei

Busting the Retirement LiesKim D. H. ButlerPreț: 68.91 lei -

How to Manage Your Money When You Don't Have AnyMR Erik WecksPreț: 83.06 lei

How to Manage Your Money When You Don't Have AnyMR Erik WecksPreț: 83.06 lei -

Stop Surviving! Start Thriving!Ashley M. MeecePreț: 65.02 lei

Stop Surviving! Start Thriving!Ashley M. MeecePreț: 65.02 lei -

The Money 20Cfp(r) Linda SchoenfeldPreț: 52.10 lei

The Money 20Cfp(r) Linda SchoenfeldPreț: 52.10 lei -

Stock Market 3 in 1 Book BundleRichard SmithsPreț: 67.69 lei

Stock Market 3 in 1 Book BundleRichard SmithsPreț: 67.69 lei -

Seven Steps to Retirement SuccessWinter a. TroxelPreț: 70.54 lei

Seven Steps to Retirement SuccessWinter a. TroxelPreț: 70.54 lei -

The New Black PowerDr Boyce D. WatkinsPreț: 170.64 lei

The New Black PowerDr Boyce D. WatkinsPreț: 170.64 lei -

Forex for BeginnersAndrew C. EllisPreț: 90.39 lei

Forex for BeginnersAndrew C. EllisPreț: 90.39 lei -

Building Wealth and Being HappyFalco, GraemePreț: 110.42 lei

Building Wealth and Being HappyFalco, GraemePreț: 110.42 lei -

7 Financial Cheat CodesHuggins, Michael A.Preț: 129.83 lei

7 Financial Cheat CodesHuggins, Michael A.Preț: 129.83 lei -

Preț: 137.30 lei

Preț: 137.30 lei -

The Game in Wall StreetHoylePreț: 61.60 lei

The Game in Wall StreetHoylePreț: 61.60 lei -

Preț: 88.41 lei

Preț: 88.41 lei -

Preț: 91.09 lei

Preț: 91.09 lei -

What Super Traders Don't Want You to KnowMustapha, AzeezPreț: 65.15 lei

What Super Traders Don't Want You to KnowMustapha, AzeezPreț: 65.15 lei -

Credit Score RepairDana LeePreț: 77.26 lei

Credit Score RepairDana LeePreț: 77.26 lei -

The Wealth Reference GuideSmith, HendrithPreț: 132.59 lei

The Wealth Reference GuideSmith, HendrithPreț: 132.59 lei

Notă biografică

Suze Orman has been called “a force in the world of personal finance” and a “one-woman financial advice powerhouse” by USA Today. A two-time Emmy Award–winning television host, #1 New York Times bestselling author, magazine and online columnist, writer/producer, and one of the top motivational speakers in the world today, Orman is undeniably America’s most recognized expert on personal finance.

Orman has written seven consecutive New York Times bestsellers and has written, co-produced, and hosted six PBS specials based on her books. She is the host of the award-winning Suze Orman Show, which airs on CNBC and XM and Sirius radio, and a contributing editor to O: The Oprah Magazine.

Orman was twice named one of the “Time 100,” Time magazine’s list of the world’s most influential people, and was the recipient of the National Equality Award from the Human Rights Campaign. In 2009 she received an honorary doctor of humane letters degree from the University of Illinois at Urbana-Champaign.

Orman, a Certified Financial Planner™ professional, directed the Suze Orman Financial Group from 1987 to 1997, served as Vice President—Investments for Prudential Bache Securities from 1983 to 1987, and was an account executive at Merrill Lynch from 1980 to 1983. Prior to that, she worked as a waitress at the Buttercup Bakery in Berkeley, California, from 1973 to 1980.

Orman has written seven consecutive New York Times bestsellers and has written, co-produced, and hosted six PBS specials based on her books. She is the host of the award-winning Suze Orman Show, which airs on CNBC and XM and Sirius radio, and a contributing editor to O: The Oprah Magazine.

Orman was twice named one of the “Time 100,” Time magazine’s list of the world’s most influential people, and was the recipient of the National Equality Award from the Human Rights Campaign. In 2009 she received an honorary doctor of humane letters degree from the University of Illinois at Urbana-Champaign.

Orman, a Certified Financial Planner™ professional, directed the Suze Orman Financial Group from 1987 to 1997, served as Vice President—Investments for Prudential Bache Securities from 1983 to 1987, and was an account executive at Merrill Lynch from 1980 to 1983. Prior to that, she worked as a waitress at the Buttercup Bakery in Berkeley, California, from 1973 to 1980.

Extras

Chapter One

All Eyes on the Road Ahead

Exhale. The eye of the financial hurricane has passed. The storm that hit in the summer of 2008 and continued to batter the global economy and your personal finances through 2009 is slowly—ever so slowly—receding. The worst is over. You survived. We survived.

Now comes the really hard work: rebuilding.

IRAs, 401(k)s and 529 college savings plans must be rebuilt in the wake of the devastating bear market.

Budgets have to be put in place that account for the new world order in which the penalties for having credit card debt and no emergency savings are unthinkable. You know as well as I do: You must find a way to get rid of the debt and build your savings.

Your approach to homeownership must be rebuilt to reflect this simple truth: A home is not a liquid investment that will always rise in value. It is shelter, first and foremost. It can also be a terrific asset, but only if you approach it with clear-eyed expectations.

Most important, your sense of security must be rebuilt. There’s the not so small issue of our collective national bill for what has happened; the current $1.4 trillion federal deficit is expected to rise to $9 trillion by 2019. But on a more personal note you are grappling with the realization that your pre-crash way of life is over. What worked—or more correctly, what you thought worked—is gone, leaving you without your bearings in these new times.

Now that we have weathered the worst of the storm, you’re onto the next challenge: Where do we go from here?

Toward Lasting Security

When I wrote the original Action Plan for 2009, it was with a laser focus on getting you through the crisis as it was unfolding. My goal was to give you the tools to find your footing in a world where the ground was shifting—and shifting violently— beneath you. As the year progressed and I heard from so many of you—in person, via Twitter, and through my CNBC show—I realized that you were hungry for more than crisis-management strategies. You have moved on to future management. You want to know the right actions to take in order to build lasting security.

You have been shaken to your core. Whether it is because of fear, regret, or remorse, living through the tumult of the financial meltdown has given you newfound purpose. You want to be in control, you want to get it right. No more fly-by-the-seat-of-your-pants, enjoy-the-ride-while-it-lasts mentality. No more trusting that things will work out, that someone else—your financial advisor, the regulators in Washington—have your back. You understand what is at stake. You are personally accountable and responsible for building and sustaining financial security. You just need a new game plan to transform your resolve into reality.

New Rules for New Times

Because so much has changed in the world and in your worldview, I decided to publish a new Action Plan. I think of it as Action Plan v. 2.0: The Long-Term View. I have updated the information and advice to take into account changes that have occurred since the fall of 2008, such as new pro-consumer credit card legislation and the Treasury Department’s broad Making Home Affordable initiative designed to keep more Americans from losing their homes. Each chapter now begins with a fresh introduction focused on “New Rules for New Times.” During the heat of the crisis my advice was to show you how to keep your money safe and secure. That’s still in play, of course, but now it’s time to move forward with strategies that will build security for you this year, next year, and beyond. That requires an understanding of what works now—and what doesn’t—in every aspect of your financial life, from credit management to retirement planning to saving for a child’s college education.

Three universal rules govern all the specific advice in the following chapters:

Rule #1: Let go of the past. There is no way you can move forward if you are still holding on to what “used to be.” As in: “My 401(k) used to be worth . . .” or “My house used to be valued at . . .” or “My job used to be secure” or “My credit card rate used to be 5%.” You can’t get where you want to go—where you need to go—if you are looking in the rearview mirror. All eyes on the road ahead. All decisions must be based on what is real today, not what used to be.

Rule #2: Plan on moderation. As I write this in the fall of 2009, the tea leaves suggest that the official recession is over and the recovery is beginning to gain momentum. But it will be a recovery of moderation, a state of affairs that has been dubbed “the new normal.” Instead of growing at the 3% annual clip that persisted for the past few decades, Gross Domestic Product (GDP) is expected to rise at a more moderate 2% rate in the new normal. That slower growth will ripple throughout the economy and your finances. Stock returns are expected to be more moderate, as are the prospects for home values. And without a booming economy, higher unemployment could be a fixture of the new normal; businesses are expected to take a slow-go approach to increasing their payroll as they grapple with the ramifications of more moderate growth and profits. New times indeed.

I also want you to understand that while the worst is over, we are not completely out of the woods. To repeat what I said a year ago: I expect we will be on a roller coaster until 2014 or 2015, because the markets, the economy, and the entire global financial system will need time to fully digest the toxic assets that still abound on many balance sheets.

Rule #3: Respect risk. Absent from the conversation throughout the stock and real estate bubbles was this crucial calculation: “What is the risk?” It’s as if everyone refused to entertain the possibility that risk existed. During the Internet stock bubble, you bought into the argument that we were at the dawn of paradigm shift—remember how often we heard that one?—that would see market gains more than double the historical rate and sustain them. When the 2000–2003 bear market hit, you were shocked—shocked!—to see your stock portfolio get creamed. And it never occurred to you, during the real estate bubble, that home values would ever—could ever—fall. It wasn’t just you; the trends and data Wall Street used to fuel much of the real estate mania didn’t even address the possibility that home values could decline! And let’s just say that Washington regulators also seemed to be asleep at the wheel in terms of managing systemic risk.

So much of the carnage could have been avoided if every one of us—individuals and institutions—had respected risk. Notice I said respect, not avoid. The goal is to stop at every juncture and make sure you understand the potential risk, and then make a conscious and deliberate decision on how to mitigate that risk. Owning a home is very risky when done with an exotic mortgage whose initial rate is artificially low but can skyrocket when it resets. Owning a home with a fixed-rate mortgage in which the monthly amount due is the same in month one as in month 360 (30 years down the line) is a whole lot less risky. An IRA invested 100% in stocks when you are in your 50s or 60s is very risky. An IRA that holds bonds and cash is a whole lot less risky.

The call to action is that you must be your own risk manager. Yes, we all should expect Washington regulators to do a better job, and let’s hope they will. But you can’t afford to rely on this; you must assess your own tolearnce for risk and understand the stakes. Your own resolve and vigilance will keep you from being hoodwinked by the next bubble. That’s right—I said the next bubble. Bubbles have long been a part of our history, for better or worse. That doesn’t mean they have to threaten your financial life; it is up to you whether you buy into them or choose to watch from the sidelines.

All Eyes on the Road Ahead

Exhale. The eye of the financial hurricane has passed. The storm that hit in the summer of 2008 and continued to batter the global economy and your personal finances through 2009 is slowly—ever so slowly—receding. The worst is over. You survived. We survived.

Now comes the really hard work: rebuilding.

IRAs, 401(k)s and 529 college savings plans must be rebuilt in the wake of the devastating bear market.

Budgets have to be put in place that account for the new world order in which the penalties for having credit card debt and no emergency savings are unthinkable. You know as well as I do: You must find a way to get rid of the debt and build your savings.

Your approach to homeownership must be rebuilt to reflect this simple truth: A home is not a liquid investment that will always rise in value. It is shelter, first and foremost. It can also be a terrific asset, but only if you approach it with clear-eyed expectations.

Most important, your sense of security must be rebuilt. There’s the not so small issue of our collective national bill for what has happened; the current $1.4 trillion federal deficit is expected to rise to $9 trillion by 2019. But on a more personal note you are grappling with the realization that your pre-crash way of life is over. What worked—or more correctly, what you thought worked—is gone, leaving you without your bearings in these new times.

Now that we have weathered the worst of the storm, you’re onto the next challenge: Where do we go from here?

Toward Lasting Security

When I wrote the original Action Plan for 2009, it was with a laser focus on getting you through the crisis as it was unfolding. My goal was to give you the tools to find your footing in a world where the ground was shifting—and shifting violently— beneath you. As the year progressed and I heard from so many of you—in person, via Twitter, and through my CNBC show—I realized that you were hungry for more than crisis-management strategies. You have moved on to future management. You want to know the right actions to take in order to build lasting security.

You have been shaken to your core. Whether it is because of fear, regret, or remorse, living through the tumult of the financial meltdown has given you newfound purpose. You want to be in control, you want to get it right. No more fly-by-the-seat-of-your-pants, enjoy-the-ride-while-it-lasts mentality. No more trusting that things will work out, that someone else—your financial advisor, the regulators in Washington—have your back. You understand what is at stake. You are personally accountable and responsible for building and sustaining financial security. You just need a new game plan to transform your resolve into reality.

New Rules for New Times

Because so much has changed in the world and in your worldview, I decided to publish a new Action Plan. I think of it as Action Plan v. 2.0: The Long-Term View. I have updated the information and advice to take into account changes that have occurred since the fall of 2008, such as new pro-consumer credit card legislation and the Treasury Department’s broad Making Home Affordable initiative designed to keep more Americans from losing their homes. Each chapter now begins with a fresh introduction focused on “New Rules for New Times.” During the heat of the crisis my advice was to show you how to keep your money safe and secure. That’s still in play, of course, but now it’s time to move forward with strategies that will build security for you this year, next year, and beyond. That requires an understanding of what works now—and what doesn’t—in every aspect of your financial life, from credit management to retirement planning to saving for a child’s college education.

Three universal rules govern all the specific advice in the following chapters:

Rule #1: Let go of the past. There is no way you can move forward if you are still holding on to what “used to be.” As in: “My 401(k) used to be worth . . .” or “My house used to be valued at . . .” or “My job used to be secure” or “My credit card rate used to be 5%.” You can’t get where you want to go—where you need to go—if you are looking in the rearview mirror. All eyes on the road ahead. All decisions must be based on what is real today, not what used to be.

Rule #2: Plan on moderation. As I write this in the fall of 2009, the tea leaves suggest that the official recession is over and the recovery is beginning to gain momentum. But it will be a recovery of moderation, a state of affairs that has been dubbed “the new normal.” Instead of growing at the 3% annual clip that persisted for the past few decades, Gross Domestic Product (GDP) is expected to rise at a more moderate 2% rate in the new normal. That slower growth will ripple throughout the economy and your finances. Stock returns are expected to be more moderate, as are the prospects for home values. And without a booming economy, higher unemployment could be a fixture of the new normal; businesses are expected to take a slow-go approach to increasing their payroll as they grapple with the ramifications of more moderate growth and profits. New times indeed.

I also want you to understand that while the worst is over, we are not completely out of the woods. To repeat what I said a year ago: I expect we will be on a roller coaster until 2014 or 2015, because the markets, the economy, and the entire global financial system will need time to fully digest the toxic assets that still abound on many balance sheets.

Rule #3: Respect risk. Absent from the conversation throughout the stock and real estate bubbles was this crucial calculation: “What is the risk?” It’s as if everyone refused to entertain the possibility that risk existed. During the Internet stock bubble, you bought into the argument that we were at the dawn of paradigm shift—remember how often we heard that one?—that would see market gains more than double the historical rate and sustain them. When the 2000–2003 bear market hit, you were shocked—shocked!—to see your stock portfolio get creamed. And it never occurred to you, during the real estate bubble, that home values would ever—could ever—fall. It wasn’t just you; the trends and data Wall Street used to fuel much of the real estate mania didn’t even address the possibility that home values could decline! And let’s just say that Washington regulators also seemed to be asleep at the wheel in terms of managing systemic risk.

So much of the carnage could have been avoided if every one of us—individuals and institutions—had respected risk. Notice I said respect, not avoid. The goal is to stop at every juncture and make sure you understand the potential risk, and then make a conscious and deliberate decision on how to mitigate that risk. Owning a home is very risky when done with an exotic mortgage whose initial rate is artificially low but can skyrocket when it resets. Owning a home with a fixed-rate mortgage in which the monthly amount due is the same in month one as in month 360 (30 years down the line) is a whole lot less risky. An IRA invested 100% in stocks when you are in your 50s or 60s is very risky. An IRA that holds bonds and cash is a whole lot less risky.

The call to action is that you must be your own risk manager. Yes, we all should expect Washington regulators to do a better job, and let’s hope they will. But you can’t afford to rely on this; you must assess your own tolearnce for risk and understand the stakes. Your own resolve and vigilance will keep you from being hoodwinked by the next bubble. That’s right—I said the next bubble. Bubbles have long been a part of our history, for better or worse. That doesn’t mean they have to threaten your financial life; it is up to you whether you buy into them or choose to watch from the sidelines.

Descriere

The nation's go-to expert on financial matters helps readers with a financial plan of action and answers their questions about credit, retirement, savings and spending, real estate, and much more. Orman delivers honest, straightforward guidance. Original.